Blog Category: Academics

“When I endeavor to examine my own conduct… I divide myself, as it were, into two persons… The first is the spectator… The second is the agent, the person whom I properly call myself.”

— Adam Smith, The Theory of Moral Sentiments, 1759

In 1759, Adam Smith set out the idea of the impartial spectator — the disciplined act of stepping outside oneself to judge one’s own conduct with honesty and without self-deception. More than two and a half centuries later, this wisdom remains entirely valid.

I write this letter in that spirit: not as an adversary, but as someone deeply convinced that the IMF possesses the knowledge, the leverage, and the convening power that — combined with willing and committed governments — can meaningfully improve lives across our continent.

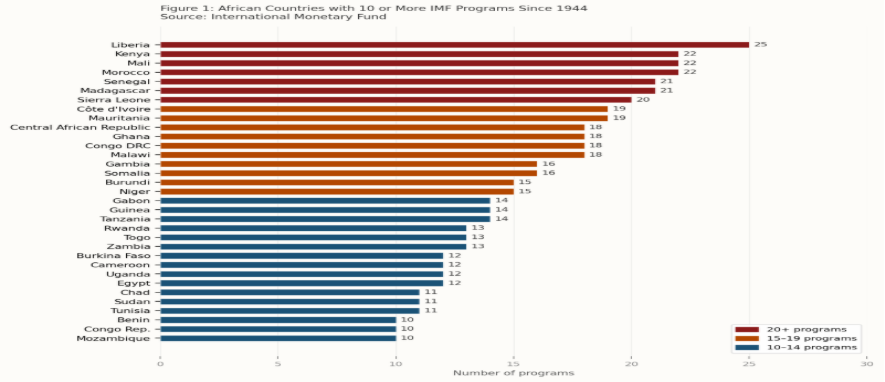

The IMF’s engagement in Africa is not modest. Since the institution’s founding, 33 African countries have each been through 10 or more IMF programs. Eight of those have been through 20 or more. Figure 1 shows every country above that threshold.

An impartial spectator looking at this frequency of intervention would naturally raise questions about effectiveness. At the recent Spring Meetings, Abebe Aemro Selassie — then-Director of the African Department — was asked what could be done to break the cycle of recurring programs.

He answered that this was a matter for governments and civil society. He is right — but the IMF carries its own agency in designing programs that succeed in light of realities on the ground, and in holding itself to the standards an impartial spectator would demand.

The following four proposals seek to close the gap between the institution’s considerable capabilities and the outcomes the evidence shows.

“If a man owes a loan and a storm destroys the grain, the harvest fails, or the grain does not grow for lack of water, then in that year he does not have to deliver grain to the creditor.” — Article 48, Code of Hammurabi, King of Babylon, c. 1750 BC

Hammurabi understood that a debtor cannot be held to the same terms when circumstances beyond his control have destroyed his capacity to pay.

During COVID-19, African governments requested exactly this: a temporary standstill on debt service for crises not of their making. The response was emergency loans and Special Drawing Rights (SDR) allocations — additional debt instruments. Countries with limited fiscal space were not relieved of their burden; they were given new instruments to manage it.

I propose that the IMF develop — and champion within the G20 and Paris Club — a rules-based framework for automatic debt service standstills triggered by qualifying external shocks: pandemics meeting World Health Organization (WHO) emergency classification, commodity price collapses exceeding defined thresholds, or climate disasters above a measurable damage-to-gross domestic product (GDP) ratio. The criteria should be objective, pre-agreed, and independent of case-by-case negotiation. Standstills, not additional loans, should be the first instrument of relief when the storm is not the borrower’s making.

The debt-to-GDP ratio tells you what a country owes relative to what it earns in a year. It says nothing about what the country owns. As Paul Sheard, former vice chairman of S&P Global, writes in The Power of Money, “this is a very misleading statistic… it divides stock, something measured in dollars, by a flow, something measured by dollars per year.”

African governments carry substantial sovereign assets this ratio systematically ignores: mineral and hydrocarbon reserves, urban land, public real estate, infrastructure, and state enterprises. Excluding them produces a distorted picture of net creditworthiness and inflates perceived debt distress.

New Zealand understood this. It measures debt sustainability on debt to net worth — the difference between its assets and debts. New Zealand pioneered this approach — hardly a far-fetched model, given that the same country gave the world central bank independence through the Reserve Bank of New Zealand Act of 1989, a reform the IMF subsequently adopted as the global standard. The IMF should now lead a similar transition for debt sustainability assessment. It is simply a fairer measure, and fairness to the countries the Fund serves should be reason enough.

This proposal, however, depends on Proposal 3: a country cannot produce a credible sovereign balance sheet without first having a functioning fiscal transparency infrastructure.

A root cause of recurring programs is the absence of basic fiscal visibility. The Public Expenditure and Financial Accountability (PEFA) framework — co-sponsored by the IMF — measures that visibility across seven pillars. The pattern across 32 African countries is shown in Figure 2.

Below Basic scores dominate the chart. The worst performance clusters in the pillars that matter most for program integrity: Assets & Liabilities, where governments cannot track or value public investment; Accounting & Reporting, where financial data integrity cannot be certified; and External Scrutiny, where audit institutions lack the independence to carry out impartial audit of government performance. Transparency and Execution Control are only marginally better. Budget Reliability — the most foundational pillar — is the least weak, yet still fails the majority.

Countries with the deepest IMF program histories — Liberia (25 programs), Madagascar and Senegal (21 each) — continue to score Below Basic across most pillars. The programs have not built the systems their own conditionality presupposes.

0 comment(s)

Leave a Comment